Latest GDP data shows Hungary’s economy is growing faster than ever

Latest GDP data shows Hungary’s economy is growing faster than ever

Official communication made us think that 4Q21 activity would be strong, and yet it is beyond expectation. The 7.1% GDP growth in 2021 is faster than ever

Hungarian economic activity shifts gear

Expectations were already high regarding Hungary's fourth-quarter GDP data, with government officials raising our expectations with their recent commentary. And yet, actual GDP growth in Q4 came in even higher than ING’s optimistic expectation which was already way above the market consensus.

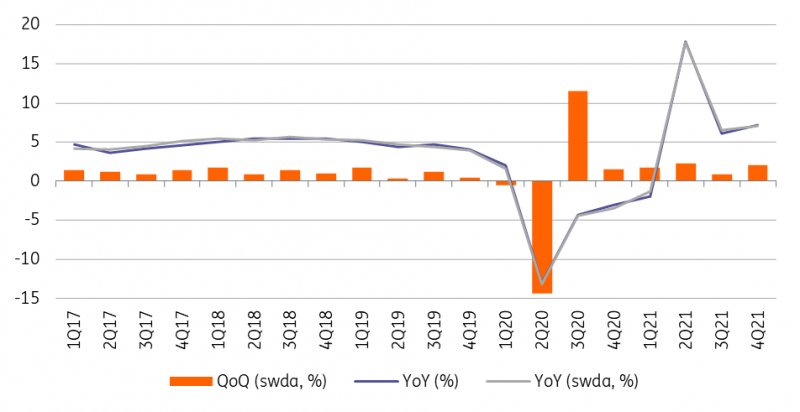

The Hungarian economy put together a 2.1% quarter-on-quarter GDP growth in the October-December period. This is the second-fastest quarterly rise – not counting the extreme post-lockdown rebound. On a yearly basis, the volume of GDP was up by 7.2% in 4Q21. This also means that Hungary is now 4% above its pre-crisis level in terms of real GDP. Last but not least, 2021 economic activity shows a 7.1% rise which is the highest in the modern era of Hungarian statistics, providing comparable GDP data from 1995.

Hungary’s real GDP growth

When it comes to the details, the Hungarian Central Statistical Office didn’t share too much in its flash report. Full detail will be released on 2 March. The statement did highlight that the most important positive contributor was the services sector, but this hardly gives us any hint about the “x-factors” which provided the upside surprise in GDP growth.

In our view, the service sector probably expanded faster than we thought based on the strong retail sector performance. Another surprise factor may have been industry and construction. Based on the monthly data publicly available, we saw nice growth in output despite the shortage economy limiting the production capacity of these sectors. It is possible that these constraints have not proved so strong in terms of added value. Based on all this, it is almost certain that the GDP growth was driven by a further recovery in consumption and, presumably, investment. Meanwhile, perhaps a slightly better industrial export performance may have constrained the negative impact of shrinking net exports on economic growth.

What does this strong finish mean for 2022?

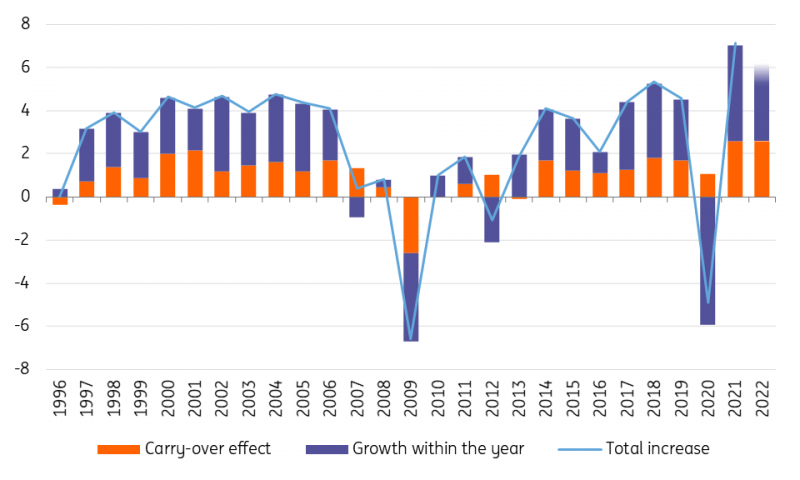

The stronger-than-expected fourth-quarter performance also means that the so-called carry-over effect is much stronger. Conceptually, carry-over effects denote the annual average rate of growth that would result if the level of GDP reached in the fourth quarter of a given year were to remain constant throughout the subsequent year. Using the market consensus (1.2% quarterly growth in Q4), the carry-over effect would have added 1.9ppt to 2022 GDP growth. Calculating the actual 2.1% quarterly rise during the fourth quarter of 2021, this carry-over effect moves up to 2.6ppt. So, the stronger-than-expected finish alone improves the 2022 GDP outlook by roughly 0.7ppt. Against this backdrop, we see a realistic shot at an above 6% GDP growth in 2022, instead of our previous 5.5% forecast.

Decomposition of Hungary's real GDP growth (% YoY)

The 2022 "carry-over effect" is calculated from the flash GDP estimate, while the "growth within the year" is based on ING forecast (gradience reflects uncertainty)

Monetary policy might need to react

The combination of today's surprisingly strong GDP data and the January inflation shock could encourage the National Bank of Hungary to continue its tightening cycle, perhaps even longer than previously expected. At present, the global supply problems do not seem to be resolving, while the Hungarian economy is showing an increasingly strong demand expansion, which will only be further heated by the government measures at the beginning of the year. Based on the latest data, we are getting closer to a scenario where both GDP growth and inflation could be above 6% on average this year. This could lead the central bank to set the terminal rate above 6% as well, instead of our latest base case of 5.5%.

Author:

Peter Virovacz

Senior Economist, Hungary

Original article: https://think.ing.com/snaps/latest-gdp-data-shows-hungary-economy-is-growing-faster-than-ever